- Premium Credit’s Insurance Index shows 70% of adults use some form of credit to pay for one or more types of cover

- Credit cards are the most used form of borrowing ahead of finance from insurers and premium finance providers

More insurance customers using credit to buy their cover are increasing the amount they borrow to help ease cost of living pressures, new research from the UK’s leading premium finance company, Premium Credit, shows.

Premium Credit’s Insurance Index*, now in its fourth year, found that nearly two out of five (38%) customers who use some form of credit to pay for one or more insurance policies borrowed more than they had in the previous 12 months for this purpose. Around half (49%) say they have not borrowed more while 3% say they have borrowed less and 10% didn’t know.

That is an increase on the one in three (34%)** borrowing more as reported by the index in March 2022 and the one in four recorded by the index*** in October 2021. The number of people using some form of credit to pay for one or more insurance policy was also higher at 70% compared with 66% in March 2022 and 69% in October 2021.

Premium Credit is seeing an increase in customers opting for finance to afford insurance – data**** from Confused.com, for instance, shows average car insurance premiums have increased 20% to a 12-year high of £657 in the first quarter of this year.

The biggest driver for increasing borrowing identified by Premium Credit’s research among those who use credit to buy insurance was the ongoing cost of living squeeze. Around 44% said they borrowed more to ease financial pressures. Just one in six (16%) said they borrowed more because of rising premiums while 6% said their income had fallen and 3% said they had lost their job.

Around 6% who used credit to pay for one or more insurance policy said they had defaulted on repayments during the past year which is slightly up on the 5% who said they had defaulted in 2022.

The number of customers cancelling policies as a result of not being able to afford cover has remained largely unchanged. Around 3% said they have cancelled contents cover – the same result as in 2022 – while around 4% have cancelled buildings cover which was slightly up on 3% in the previous index.

Premium Credit’s Insurance Index, which monitors insurance buying and how it is financed, found the use of different forms of borrowing remained unchanged. Credit cards remain the most popular form of borrowing used by 35% which was unchanged on the previous year while 27% rely on finance offered by their insurer and/or premium finance provider which was also the same in last year’s index.

The numbers using personal loans and borrowing from family and friends dropped slightly from 9% and 7% in the 2022 index to 8% and 6% this year. Around 4% relied on high interest loans.

Premium Credit is advising customers to consider premium finance which, for a small charge, enables them to pay monthly for cover instead of in a lump sum. Spreading payments in such a way can help ease cash flow challenges and make paying for vital insurance more convenient.

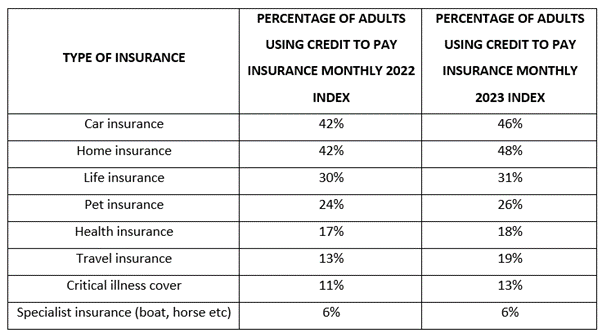

Its study shows widespread use of credit by consumers, as the table below demonstrates, with numbers rising across all types of insurance monitored apart from specialist insurance. The biggest rise was in travel insurance.

Adam Morghem, Premium Credit’s Strategy, Marketing & Communications Director said: “The ongoing economic strain and cost of living crisis is having an impact on borrowing to fund insurance with total numbers using credit rising.

“Premium finance is specifically designed for personal and commercial insurance buyers to help make important insurance policies affordable and improve cashflow. Looking to spread the cost of an annual policy into more manageable monthly payments works for many millions of UK consumers and businesses.

“It is a very cost-competitive means for consumers to buy insurance and better manage their finances through spreading payments. At a time when household finances are under pressure it can be a good alternative to other forms of credit like credit cards or bank over drafts.”

Premium Credit’s research highlighted the cost of not having the right insurance – around one in twelve (8%) of those who use credit to pay for insurance have not been able to make claims in the past five years either because they had no cover or had inadequate cover. Nearly two out of three (67%) lost out on claims worth £1,000 or more.

Notes to editors:

* Independent consumer research conducted by Viewsbank among a nationally representative sample of 1,106 aged 18-plus between March 10th and 12th 2023

** Independent consumer research conducted by Viewsbank among a nationally representative sample of 1,026 aged 18-plus between March 11th and 13th 2022

*** Independent consumer research conducted by Viewsbank online among a nationally representative sample of 1,017 adults aged 18-plus between October 1st and 4th 2021

**** Car insurance price index - Confused.com

For further information please call Phil Anderson at Perception Aon 07767 491 519